You are now leaving the Alexander Peter Wealth Management Global website and being redirected to the Alexander Peter Wealth UK website. The Alexander Peter Wealth UK website is designed for UK residents only and may include products and services that are not covered in your region.

You are now leaving the Alexander Peter Wealth Management Global website and being redirected to the Alexander Peter Wealth Management USA website. The Alexander Peter Wealth Management USA website is designed for US residents only and may include products and services that are not covered in your region.

What happens to your UK State Pension if you’re a British expat?

Alex Stojkovic

|

Pensions

|

January 21, 2026

There’s a good chance that, when you were living and working in the UK, you likely understood that you were entitled to the State Pension if you met certain criteria.

The guaranteed State Pension payment could be a valuable source of income during the next phase of your life.

Yet, if you’ve since moved abroad, you may not be entirely certain what happens to your State Pension.

Unlike private or workplace pensions, the UK State Pension is tied by often complex rules depending on where you now live.

Keep reading to find out exactly what happens to your State Pension as an expat, and how understanding the rules could boost your financial security in retirement.

You’re still typically entitled to the State Pension as an expat

First, it’s vital to remember that you are still entitled to the State Pension when you move abroad.

To qualify for the new State Pension, you typically need at least 10 qualifying years on your National Insurance (NI) record to receive any at all, or 35 years for the full entitlement.

To accrue these qualifying years, you must have:

• Worked in the UK and made National Insurance contributions (NICs)

• Received National Insurance credits, for events such as if you were unemployed, ill, or a parent or carer

• Paid voluntary NICs.

So, just because you move abroad, doesn’t mean you lose these qualifying years and are no longer entitled to the State Pension.

Once you reach the State Pension Age (66 in 2025/26, expected to rise to 67 between 2026 and 2028), you can arrange for your entitlement to be paid directly into your overseas bank account.

The “triple lock” increases the value of the State Pension each year, but there are rules to consider

The “triple lock” is a government measure that increases the value of the State Pension each year according to the highest of:

• Inflation (as measured by the Consumer Prices Index (CPI) in September of the previous year)

• The average yearly wage increase

• 2.5%.

However, it’s vital to remember that the triple lock typically only applies to your own entitlement as an expat if you move to:

• The European Economic Area (EEA) or Switzerland

• Countries that have a social security agreement with the UK (as the government website lists) that includes uprating the State Pension. This excludes Canada and New Zealand, both of which have social security agreements with the UK that do not include pension uprating.

Otherwise, while you can still claim your State Pension, the amount will remain unchanged, regardless of triple lock rises.

MoneyWeek reveals that these rules have caught out many.

Indeed, someone who retired to a country 15 years ago, where the UK State Pension has not risen according to the triple lock, would have had their annual entitlement frozen at £5,077.

A pensioner living in the UK would have received the same amount in 2010, but the amount they were receiving would have increased each year. Over 15 years, lost State Pension entitlement for expats would have amounted to £25,832.

Remember that the State Pension typically won’t be enough to fund a comfortable retirement

This loss of income can undoubtedly be frustrating, as every little helps when it comes to securing your dream retirement.

That said, it’s likely that the full new State Pension wouldn’t be enough to entirely fund your ideal lifestyle when you stop working.

As of 2025/26, the full State Pension stands at £230.25 a week, or £11,973 a year. Yet, the Pension and Lifetime Savings Association suggests that a single person would need around £43,900 a year to support a comfortable retirement. For a couple, that figure rises to £60,600.

This is why it’s so important to bolster the size of your private pension whenever possible, especially as an expat.

One of the more effective – and arguably simplest – steps you can take is to increase your pension contributions.

Even minor adjustments now could, over time, make a significant difference.

If your income rises, you may want to consider increasing your pension contributions. This could both help you accumulate a larger fund, and potentially reduce a tax bill.

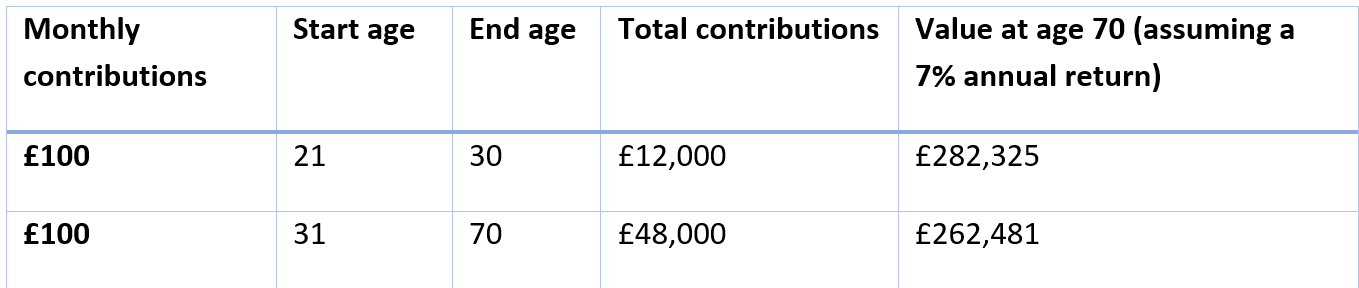

What’s more, the earlier you increase contributions, the better – this is thanks to the power of compounding, which is essentially “returns on returns”.

As you can see, if you focus on building your financial security for retirement earlier, even modest amounts can add up over time.

It’s worth speaking to a specialist financial planner

While you can navigate the complexities of cross-border retirement planning on your own, working with a planner who understands the unique challenges expats face could make a significant difference.

We specialise in helping British expats across Europe, the US, Canada, and beyond. Our expert knowledge could help you avoid making costly mistakes now and ensure you remain on track to achieve your long-term goals.

To find out more about how we might support you, please email enquiries@alexanderpeter.com or give us a call on +44 1689 493455.

Please note

This article is for general information only and does not constitute advice. The information is aimed at retail clients only.

All information is correct at the time of writing and is subject to change in the future.

A pension is a long-term investment not normally accessible until 55 (57 from April 2028). The fund value may fluctuate and can go down, which would have an impact on the level of pension benefits available. Past performance is not a reliable indicator of future performance.

The tax implications of pension withdrawals will be based on your individual circumstances. Thresholds, percentage rates, and tax legislation may change in subsequent Finance Acts.

Please do not act based on anything you might read in this article. All contents are based on our understanding of HMRC legislation, which is subject to change.

The Financial Conduct Authority does not regulate tax planning.

Thank you

We will be in touch soon.

Sorry. Something went wrong. Please try again.

Share this page

You might also be interested in:

Pensions

Your guide to the new Inheritance Tax and pension rules