You are now leaving the Alexander Peter Wealth Management Global website and being redirected to the Alexander Peter Wealth UK website. The Alexander Peter Wealth UK website is designed for UK residents only and may include products and services that are not covered in your region.

You are now leaving the Alexander Peter Wealth Management Global website and being redirected to the Alexander Peter Wealth Management USA website. The Alexander Peter Wealth Management USA website is designed for US residents only and may include products and services that are not covered in your region.

5 financial tasks to tackle now if you’re retiring in 2026

Alex Stojkovic

|

Investments

|

November 19, 2025

If you’re planning to retire in 2026, you may have only a few short months of work left until you can start to enjoy the fruits of your labour.

Whether you’re planning to travel, take up a new hobby, or simply spend more quality time with your family, retirement presents a whole new chapter of life to look forward to.

As well as planning all the lovely ways to use your free time, there are a few financial to-dos that could be very useful to complete before you finish work.

Read on to discover five simple tasks that could help ensure your finances are in good shape before you take the first steps into your exciting next chapter.

1. Trace any lost pension pots

If you’ve worked for several different companies in different locations around the world during your career, you may have multiple pension pots to your name and could have forgotten funds along the way.

If you think you have pension pots in the UK, you can use the government’s pension tracing service to discover the details for your funds. Once located, log in and update your contact details.

In other countries, start by contacting your former employer to ask for details of the company scheme. Then, you can go directly to the pension provider, update your contact details, and request an up-to-date statement.

Reclaiming lost pension pots could add a significant boost to your existing savings. Pensions UK reports that there could be a combined £31.1 billion sitting in lost pension pots in the UK alone, with an average of £9,470 in each fund.

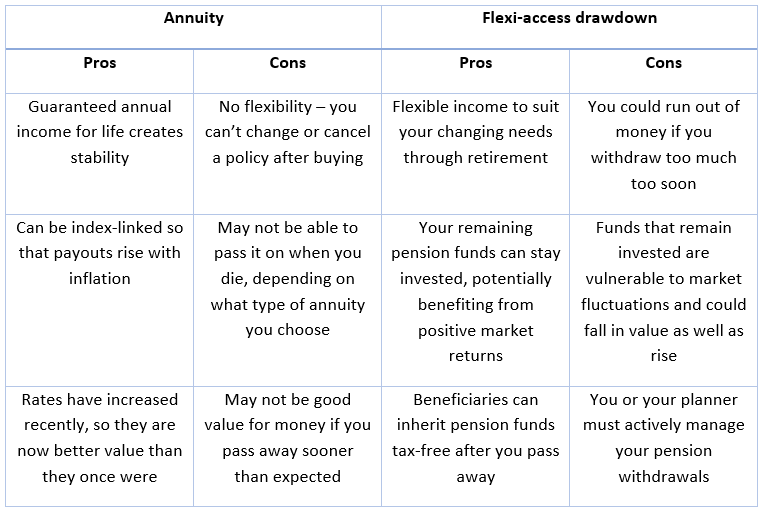

2. Consider how you’d like to take your income in retirement

There are multiple methods you can use to access your retirement savings.

As well as the option of buying an annuity when you retire, you can also consider taking a flexible income using drawdown. This allows you to withdraw funds from your pension as and when you need to.

The table below shows the key pros and cons for each approach.

Alternatively, you could consider a mix-and-match approach by buying an annuity with some of your pension funds and leaving the rest invested for flexible access through drawdown.

While you may consider your pension as the foundation of your retirement plan, if you have other income that uses your tax allowances, it may be wiser to spend this money and delay drawing on your pension.

The order, timing, and structure of income withdrawals can make or break your long-term plan.

For expert support, please get in touch. We can help you devise a tax-efficient and sustainable income structure based on your circumstances and goals.

3. Understand how much you may receive from the UK State Pension or other government schemes

If you’re a British expat, you may qualify for the UK State Pension, as well as social security payments in your country of residence.

For example, if you’ve worked in the US for at least 10 years, you are likely eligible to receive US Social Security benefits.

The longer you’ve worked and the higher your earnings, the more you’ll receive – up to a current maximum of around $50,000 a year.

Meanwhile, to qualify for a full UK State Pension, you need at least 35 qualifying years of National Insurance contributions. The full pension is currently worth just under £12,000 a year and, depending on where you live, rises with inflation.

Even if you only lived in the UK for part of your career, you may still be eligible. You may also be able to top up missing years voluntarily.

Depending on your age, you’ll normally receive your UK State Pension from age 66, rising to 67 between May 2026 and March 2028. To find out how much you might receive, get your State Pension forecast from the government’s website.

Wherever you reside, if you expect to receive multiple pension payments, you’ll need to consider:

When to begin claiming each pension to maximise value

How the income may impact your tax bracket

Exchange rates when planning withdrawals or converting income.

State pension payments can be a strong foundation for your retirement, but without proper planning, they can create confusion, delays, or tax inefficiencies.

4. Make sure your estate plan is up to date

Your retirement can be a good time to review your estate plan and ensure it is up to date. This might include your:

Will

Expression of wish form

Lasting Power of Attorney(s)

In Case of Emergency (ICE) document.

Keeping these documents up to date can help to lessen the impact of any difficulties you may face during your retirement. You can also help your family by making it easier for them to manage your affairs and finances after you pass away.

It’s wise to meet with your planner to review your estate plan at regular intervals, and after milestone achievements such as buying or selling property, having a child or grandchild, or getting married or divorced.

Your financial planner can help you review the value of your pension funds, investments, and other savings against your expected income needs in retirement.

This means you can feel confident that you’re set up for success following your imminent change of circumstances. Additionally, your planner can help you look further ahead to anticipate how your income needs might change throughout your retirement.

When you have a clear idea of what you will need later on, you can establish a strategic and sustainable income, ensuring you’re able to enjoy yourself today while also being careful to set aside enough to pay for later-life costs.

Get in touch

If you’re looking forward to retiring in 2026, now is the time to put the right structure and strategy in place – and we’re here to help.

This article is for general information only and does not constitute advice. The information is aimed at retail clients only.

All information is correct at the time of writing and is subject to change in the future.

The Financial Conduct Authority does not regulate estate planning, tax planning, trusts, Lasting Powers of Attorney, or will writing.

A pension is a long-term investment not normally accessible until 55 (57 from April 2028). The fund value may fluctuate and can go down, which would have an impact on the level of pension benefits available. Past performance is not a reliable indicator of future performance.

The tax implications of pension withdrawals will be based on your individual circumstances. Thresholds, percentage rates, and tax legislation may change in subsequent Finance Acts.

Your pension income could also be affected by the interest rates at the time you take your benefits. The tax implications of pension withdrawals will be based on your individual circumstances, tax legislation, and regulation, which are subject to change in the future.

Workplace pensions are regulated by The Pensions Regulator.

Thank you

We will be in touch soon.

Sorry. Something went wrong. Please try again.

Share this page

You might also be interested in:

Pensions

Your guide to the new Inheritance Tax and pension rules

.jpg)