You are now leaving the Alexander Peter Wealth Management Global website and being redirected to the Alexander Peter Wealth UK website. The Alexander Peter Wealth UK website is designed for UK residents only and may include products and services that are not covered in your region.

You are now leaving the Alexander Peter Wealth Management Global website and being redirected to the Alexander Peter Wealth Management USA website. The Alexander Peter Wealth Management USA website is designed for US residents only and may include products and services that are not covered in your region.

Why investing in UK buy-to-let property isn’t the simple decision it once was

Alex Stojkovic

|

Investments

|

April 23, 2026

The cost of renting residential property in the UK has stalled. According to data from Rightmove, it’s the first time since 2017 that rents have not increased in the first three months of a year compared with levels in the final quarter of the previous year.

As affordability remains a stretch, the UK’s number one property portal says there are an increasing number of signs that tenants have maxed out the amount they can afford to pay.

And stalling rental prices isn’t the only problem UK landlords face.

Recent tax reforms, higher Stamp Duty charges, and new legislation mean that investing in property may no longer be as attractive or easy as it’s been in the past. Plus, inflationary pressures may add to price concerns and keep rental prices lower for longer.

If you own buy-to-let property or are considering investing in UK rental property, here are the key changes that could affect your potential returns, and how we may be able to offer a simple solution.

3 key tax changes that could eat into your profits

As a British expat with buy-to-let property in the UK, your overall return may be impacted by the following taxes.

1. Stamp duty surcharges might increase the cost of purchase

Thanks to Stamp Duty, the initial tax bill could be far higher than you might anticipate.

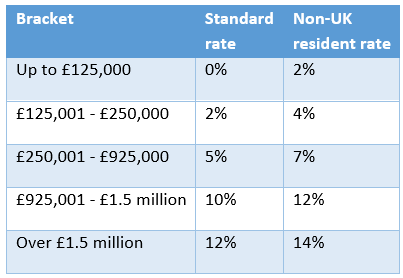

The table below shows the current Stamp Duty Land Tax (SDLT) rates:

If you’re a UK expat and don’t spend at least 183 days (six months) in the UK during the 12 months before purchasing a property, you’ll be classed as “not a UK resident” and charged the higher rate of SDLT.

Your circumstances will dictate how the calculations play out, but you could face three layers of SDLT:

The standard SDLT rate on the property purchase.

A 5% surcharge for buying an additional residential property.

A 2% surcharge applied to non-UK residents.

Any or all of these charges could add thousands of pounds to the cost of buying a rental property.

With this in mind, it’s sensible to run the numbers and check you understand all the costs involved before you invest in UK property. If in doubt, please get in touch and we’ll help with the calculations.

2. Income Tax on rental income could impact your return on investment

Even if you live abroad, money you make from renting UK property is usually subject to Income Tax at your marginal rate.

Though there are some small allowances (the £1,000 Property Allowance, for example), after deducting allowable expenses, most landlords will end up paying some tax on their rental profits.

Before 2017, you were able to deduct mortgage interest and other finance costs such as mortgage arrangement fees from your rental income, but now you receive a 20% tax credit instead.

And there’s more change on the horizon, as the rate of tax on property income is set to increase by 2% across all tax bands – to 22% for basic-rate taxpayers, 42% for higher-rate taxpayers, and 47% for additional-rate taxpayers.

3. Capital Gains Tax (CGT) may apply to any profit you make when you sell

For the 2026/27 tax year, gains on residential property are typically taxed at:

18% for gains within the basic-rate band

24% for gains above the basic-rate band.

One bit of good news: even UK expats are granted a £3,000 annual CGT allowance (2026/27), which you could use to help reduce your taxable gain.

New legislation may impact how you manage your UK property

As well as the potentially costly tax changes, the new Renters’ Rights Act will introduce significant changes for tenants and landlords.

From May 2026, new laws will give UK tenants stronger rights, better protection, and more security.

Some of these changes may alter the way you manage your rental property, most notably:

End of “no-fault” evictions – You must have a legally valid reason to evict tenants.

Fixed contracts will no longer apply – All rental agreements will roll on from month to month or week to week, and you can’t apply an end date. Tenants can give two months’ notice to end contracts.

Fairer rent rules – You’ll only be allowed to raise rent once a year, and tenants can challenge unfair hikes.

New rules will also limit how you manage rent and tenant selection. Plus, to prevent bidding wars, you must stick to the rent advertised, and you no longer have the option to allow prospective tenants to increase their offer to secure the tenancy.

All this to say, such comprehensive rule changes may make it more time-consuming and effortful to manage your UK rental property.

We can help you to tap into the value offered by UK real estate with minimal effort

Our team of investment consultants have a wealth of knowledge and experience in the property market and are always on hand to discuss the current opportunities and talk you through the investing process.

One area that may help to alleviate typical landlord headaches is investing in UK social and supported housing.

Complete and ready for investment, all properties offer turn-key solutions, while other notable benefits include:

Market-leading rental yields, backed by government returns ranging from 8-10% NET per annum

Long-term lease agreements with commercial tenants, ensuring stable rental income for 10-25 years

Comprehensive full repairing and insuring leases, simplifying your investment and removing the burden of property maintenance.

Get in touch

If you’re interested in learning more about how investing in property could help diversify your portfolio and support your long-term financial goals, please get in touch.

This article is for general information only and does not constitute advice. The information is aimed at individuals only.

All information is correct at the time of writing and is subject to change in the future.

Please do not act based on anything you might read in this article. All contents are based on our understanding of HMRC legislation, which is subject to change.

The Financial Conduct Authority does not regulate buy-to-let (pure) and commercial mortgages.

Thank you

We will be in touch soon.

Sorry. Something went wrong. Please try again.

Share this page

You might also be interested in:

Investments

Practical steps to help you or a loved one “age in place” at home

.jpg)