You are now leaving the Alexander Peter Wealth Management Global website and being redirected to the Alexander Peter Wealth UK website. The Alexander Peter Wealth UK website is designed for UK residents only and may include products and services that are not covered in your region.

You are now leaving the Alexander Peter Wealth Management Global website and being redirected to the Alexander Peter Wealth Management USA website. The Alexander Peter Wealth Management USA website is designed for US residents only and may include products and services that are not covered in your region.

Own property in the UK? Here’s how the Autumn Budget could affect you

Alex Stojkovic

|

Investments

|

January 21, 2026

Owning property in the UK has long appealed to both UK residents and overseas investors.

The 2025 Autumn Budget introduced several changes that could materially affect landlords and property owners.

From frozen tax thresholds and higher taxes on rental income to the introduction of a so-called “mansion tax”, if you live overseas but own property in the UK, these changes may apply to you.

Keep reading to find out three key changes you need to prepare for.

Extended tax threshold freezes could leave you more exposed over time

While Labour kept its promise not to increase Income Tax or National Insurance, tax thresholds will remain frozen at current levels for a further three years – until April 2031.

The Inheritance Tax (IHT) nil-rate band will also remain frozen at £325,000 until 2031.

While such freezes don’t increase tax rates directly, they do create fiscal drag. As rents, wages, and property values rise, more people could see their income and estate pulled into higher tax bands.

Separate your income streams, as tax on property income increases by 2% from April 2026

The decision to tax property income separately from other income sources is among the most significant changes for landlords.

From April 2026, income from property will be treated differently.

The new tax rates coming into force on 6 April 2026:

Property basic rate – 22%

Property higher rate – 42%

Property additional rate – 47%

This represents an effective 2% increase across each band.

If you earn income from UK property, this may be something you need to account for in the new tax year.

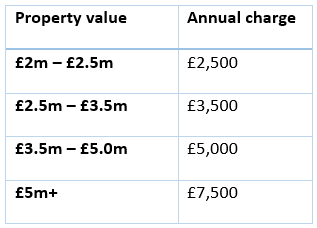

Limber up for the “mansion tax” on residential properties worth £2 million or more

An annual charge on high-value residential properties, dubbed the “mansion tax”, will apply to residential properties worth £2 million or more, from April 2028.

The charge will be based on targeted valuations and is in addition to existing Council Tax.

The new property tax will be payable by property owners, not occupiers, and is expected to raise around £430 million each year.

According to the Treasury, “fewer than 1% of properties in England are expected to be above the £2 million threshold” and “revaluations will be conducted every five years”.

If you hold premium UK residential property, this new fixed annual cost may affect your long-term returns.

Own property through a company? Watch out for the Dividend Tax increase

From April 2027, Dividend Tax will increase by 2% for basic- and higher-rate taxpayers. For additional-rate taxpayers, the rate remains unchanged.

This change will affect you if you hold your property portfolio in a company structure – if this applies to you, it may be more tax-efficient to retain profits or reinvest dividends in the business.

As the change won’t come into force until 6 April 2027, you’ve time to consider your options. If you’d like to discuss how the change will affect your financial plan, please get in touch.

It may be time to rethink how you invest in property

Higher taxes, additional charges, and evolving rules may prompt you to consider alternative ways to invest in UK property.

At Alexander Peter, we work with international clients who want access to UK property – but without the administrative burden of being a landlord.

Our team of property experts and partners are on hand to:

Research and advise on all the available opportunities and help you understand what might suit you best

Find and secure the right mortgage at the best possible rate

Source and furnish the property to your budget and specifications

Arrange, set up, and manage letting your property to tenants

Establish an appropriate structure so that you can benefit from tax efficiency now and in the future.

Get in touch

If you’d like to discuss how the changes announced in the UK Autumn Budget might affect your financial plan, or are keen to find out more about how we could help you invest in UK property, please get in touch.

This article is for general information only and does not constitute advice. The information is aimed at individuals only.

All information is correct at the time of writing and is subject to change in the future.

Please do not act based on anything you might read in this article. All contents are based on our understanding of HMRC legislation, which is subject to change.

The value of your investments (and any income from them) can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance.

Investments should be considered over the longer term and should fit in with your overall attitude to risk and financial circumstances.

Thank you

We will be in touch soon.

Sorry. Something went wrong. Please try again.

Share this page

You might also be interested in:

Pensions

Your guide to the new Inheritance Tax and pension rules

.jpg)