You are now leaving the Alexander Peter Wealth Management Global website and being redirected to the Alexander Peter Wealth UK website. The Alexander Peter Wealth UK website is designed for UK residents only and may include products and services that are not covered in your region.

You are now leaving the Alexander Peter Wealth Management Global website and being redirected to the Alexander Peter Wealth Management USA website. The Alexander Peter Wealth Management USA website is designed for US residents only and may include products and services that are not covered in your region.

How a health savings account could help expats in the US save for retirement

Alex Stojkovic

|

Investments

|

January 21, 2026

Bucket-list vacations, golf club memberships, and regular trips to visit family overseas all come at a price for expat retirees, but for those living in the US, healthcare could be the largest expense by far.

While those in the UK can fall back on the NHS, in the US, healthcare – and health insurance – is big business.

According to data from Fidelity, an average retired couple, both age 65, could need roughly $345,000 to cover the cost of healthcare in retirement.

Planning ahead for such expenses could help protect your financial security, allowing you to relax and enjoy your retirement without worrying about how you’ll pay to take care of your health.

Read on to find out how a health savings account (HSA) could be an effective and tax-efficient way to save for retirement and potentially cover long-term medical expenses.

3 tax advantages you can enjoy with a health savings account

First, it’s important to note that under IRS rules, you can only open and contribute to an HSA if you’re enrolled in a high-deductible health plan.

Although HSAs often cover higher levels of expenses, they typically have relatively low premiums, with the difference offset through funds saved in your account.

Here’s how saving through an HSA works and where you could benefit from tax-efficiencies:

Contributions to HSAs are tax-free. Contributions made through payroll deductions aren’t subject to Social Security or Medicare taxes either.

You can invest the money, and any growth is free from tax.

Withdrawals you make for qualified health expenses don’t incur taxes.

Using a health savings account to help you save for retirement

If you’re already making the most of your 401(k), an HSA can help to boost your long-term retirement planning.

While HSAs are commonly associated with covering high medical bills, they can also work as an additional retirement savings vehicle.

Unlike a flexible spending account (FSA), any money you don’t use in your HSA remains yours. You don’t lose it if you change jobs, move countries, or switch health plans.

If you later move away from a high-deductible health plan, you won’t be able to make new contributions. However, the money already in your HSA remains yours to use for qualified medical expenses whenever you need it.

Because your HSA balance can be invested, any growth has the potential to compound over decades. Alongside your 401(k) and any IRAs, your HSA could become a dedicated pot to help cover healthcare costs later in life.

The deadline to contribute to a health savings account in the 2025 tax year is 15 April 2026

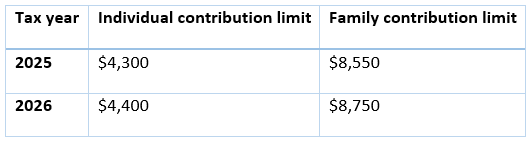

How much you can contribute to an HSA in this tax year and next:

If you’re 55 or older, you can contribute an extra $1,000 each year as a catch-up contribution in both 2025 and 2026. Plus, in some cases your employer may also contribute.

The deadline to make HSA contributions for the 2025 tax year is 15 April 2026. So, there’s still time to open or top up your HSA. If you don’t already have an HSA or would like to understand how your current HSA compares to others, please get in touch.

Using your health savings account for medical and non-medical expenses in retirement

It’s important to note that rules don’t allow you to contribute to an HSA if you’ve enrolled in Medicare.

That said, the accounts could offer new benefits in retirement. As well as using your HSA to cover qualified medical expenses, after age 65 you can also use it for non-medical expenses without penalty, though you will need to factor in tax – which will be due on withdrawals for non-medical costs.

Unlike 401(k) plans and traditional IRAs, HSAs don’t have any minimum distribution restrictions, meaning you can keep your money in the HSA until you’re ready to use it.

A health savings account could enhance your retirement strategy

An HSA can be a useful addition to your retirement plan because once your balance reaches a certain level, most providers allow you to invest the money saved in the account.

Much like a 401(k), HSA investment options are usually limited to a predefined range of funds. While this keeps things simple, it also means fees, flexibility, and investment choice can vary widely.

If you’re unhappy with the investment options or charges within your HSA – or if your employer doesn’t offer one – you can open an HSA independently. While this could allow you greater control, contributions to an HSA outside the workplace won’t benefit from automatic, pre-tax payroll deductions, and you won’t receive any employer contributions.

Instead, you’ll fund the account using post-tax income and reclaim the tax benefits when you file your return. Contributions will also be subject to Social Security and Medicare taxes.

How much you contribute, whether you invest the balance, and when you choose to spend those funds should all align with your wider retirement goals, income needs, and future healthcare expectations.

Get in touch

With the right planning, an HSA can complement your other retirement savings and help you prepare for costs that often rise later in life.

To discuss your retirement plan and how an HSA may benefit you, email enquiries@alexanderpeter.com or give us a call on +44 1689 493455.

Please note

This article is for general information only and does not constitute advice. The information is aimed at individuals only.

All information is correct at the time of writing and is subject to change in the future.

The value of your investments (and any income from them) can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance.

Investments should be considered over the longer term and should fit in with your overall attitude to risk and financial circumstances.

Thank you

We will be in touch soon.

Sorry. Something went wrong. Please try again.

Share this page

You might also be interested in:

Pensions

Your guide to the new Inheritance Tax and pension rules

.jpg)